11 / 40

11 / 40

Concentration of market power

in the EU seed market

11

The increase in size of the EU seed market and its role as the first global exporter of seed has put Europe at the

centre of the international seed sector

21

. As observed by different intergovernmental institutions and studies

at an international level, a large part of the market lies in the hands of a very small number of companies. This

consolidation has happened in the last 15-20 years, starting in the nineties

(table 1)

.

Two recent studies show that the largest 10 companies have a worldwide market share of between 62%

22

and

75.3%

23

: note that five of them are companies that produce both seeds and agro-chemicals, and the four biggest

seed giants have a total market share between 48.2% and 58.2% according to the same studies.

With Europe being the world’s leading exporter in seeds and the third biggest world market for seeds, the

question of dominance of just a few players is a highly relevant one. It would be naïve to consider that such an

important market is not highly interesting for the seed giants. Additionally, from a legislative perspective, critics

claim that

“for the past 50 years Europe has been a laboratory for seed laws that it subsequently imposes on the

entire planet through free trade agreements”

24

. Indeed, the EU has both an economic footprint on the rest of the

world because of its strong export role, and also a legislative footprint because of states outside the EU copying

its laws in order to ease trade with the block.

20. KWS 2013 data for vegetables, maize and sugar beet,

http://www.kws.de/global/show_document.asp?id=aaaaaaaaaaffxwnand

Commission staff working document

impact assessment accompanying the document proposal for a regulation of the European Parliament and of the Council on the production and making available on the

market of plant reproductive material,

European Commission, May 2013,

http://ec.europa.eu/dgs/health_consumer/pressroom/docs/proposal_aphp_ia_en.pdf21. France is currently the largest world seed exporter and the Netherlands is the third largest (

La filière des semences affiche un excédent record de 836 M d’euro

s,

Agra Presse hebdo, Semaine du 25 novembre 2013 – N° 3423).

22. Fugeray-Scarbel et Lemarie, 2013:

Évolution de l’organisation de la recherche et du secteur des semences

.23. ETC group,

Putting the Cartel before the Horse ... and Farm, Seeds, Soil, Peasants, etc. Who Will Control Agricultural Inputs?,

ETC Group, September 2013,

http://www.etcgroup.org/sites/www.etcgroup.org/files/CartelBeforeHorse11Sep2013.pdf24.

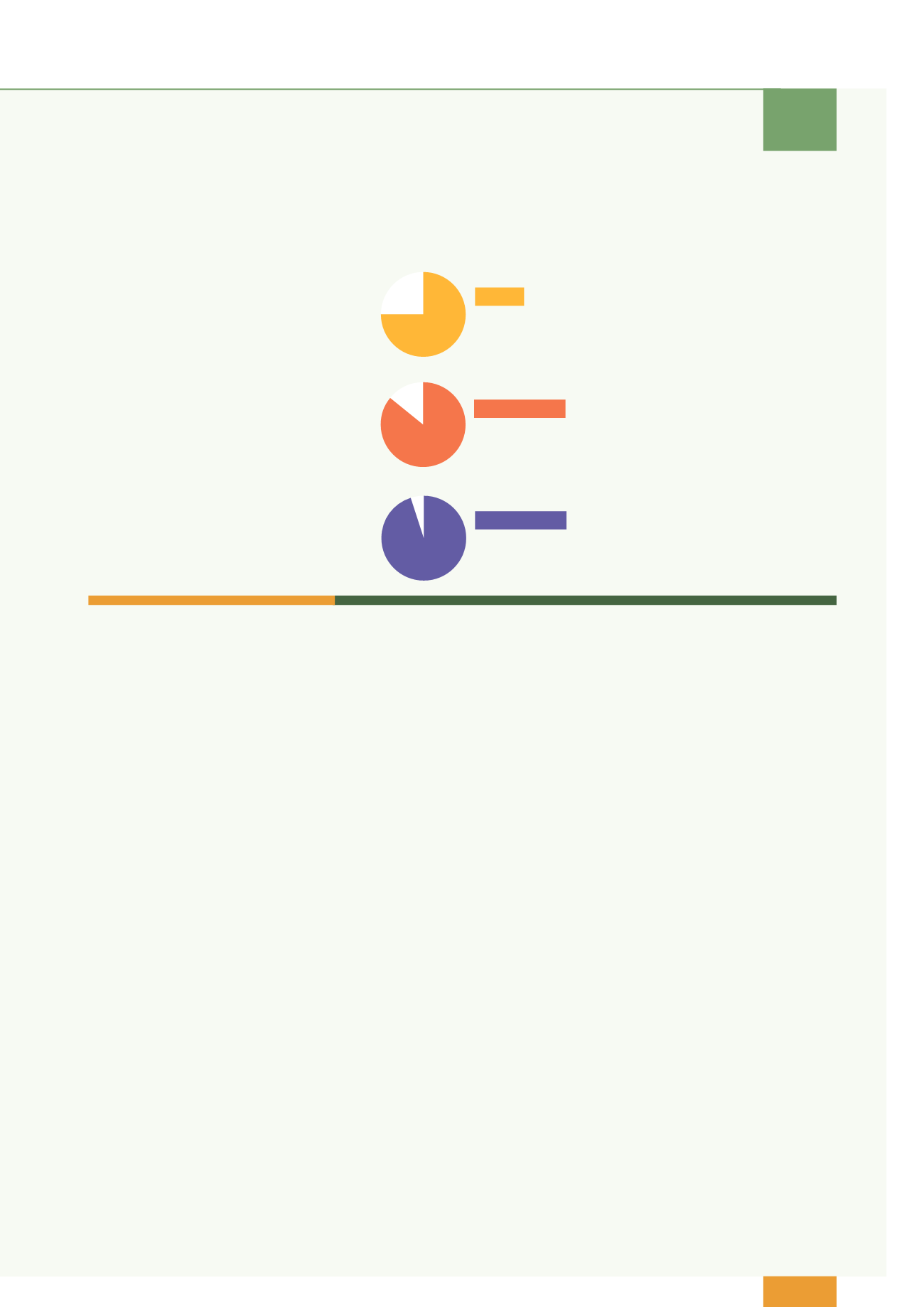

Position on the marketing of seeds, plant health and controls , European Coordination Via Campesina, December 2012, http://www.eurovia.org/spip.php?article711Based on available information on market shares, 40% of the total EU seed market co

extremely concentrated markets.

75% of market share

controlled by the top 5 companies of the sector

maize

86% of market share

controlled by the top 4 companies of the sector

Sugar beet

95% of market share

controlled by the top 5 companies of the sector

vegetables

Figure 2:

EU market shares of the top

companies in the maize, sugar beet

and vegetable seed market, for the

years 2012-2013

20

Based on available information on market sh res, 40% of the t tal EU s ed market corresponds to

extremely concentrated mark ts.

75% of market share

controlled by the top 5 companies of the sector

maize

86% of market share

controlled by the top 4 companies of the sector

Sugar beet

95% of market share

controlled by the top 5 companies of the sector

vegetables